Ways to increase the profitability of a company. Profitability - what is it and how to calculate it? Enterprise profitability and its indicators

The profitability of an enterprise is an indicator that directly affects profit, i.e., the final result of the activities of any enterprise. Increasing the profitability of an enterprise is one of the main goals of the management of any enterprise. There are many ways to increase profitability; each enterprise chooses the most suitable for a particular enterprise. Let's consider the main methods of increasing profitability and see what impact they have on the final result of financial and economic activities.

In order for an enterprise to be profitable and have a stable position in the market, it is necessary:

- produce products that are in demand. You can produce a lot of products, but if there is no demand for it, then there is no point in such production;

- sell products at a price that corresponds to the average market price and at which potential consumers are willing to purchase these products. To set such a price, enterprise specialists must study the sales market, potential consumers, their needs and payment abilities, the competitiveness of the enterprise and competitors’ prices for similar products;

- produce products in the quantity required by the market so that the product does not sit in the warehouse, especially if it has a limited shelf life;

- produce products with a rational calculation of production costs. When production costs exceed revenue from product sales, production is considered unprofitable and unprofitable, it does not make a profit. This could lead to bankruptcy.

Assessing the level of profitability

Assessing profitability involves analyzing absolute and relative indicators characterizing its level.

The absolute indicator is profit. Due to it, the enterprise can increase the wage fund, expand and increase production turnover, finance other areas of activity, etc. In general, profit is the difference between the cost of selling a product and its cost (the sum of all costs spent on the production of this product).

The amount of profit can be found out from the financial statements, namely from the financial results statement (form No. 2).

Let's look at a fragment from the financial statements for 2016 of Alpha LLC, which produces chairs (Table 1).

Table 1 Financial results report for 2016

|

Index |

Meaning |

|

Sales volume, pcs. (units) |

|

|

Price per unit, rub. |

|

|

Revenue, rub. |

|

|

Costs (cost of sales), rub. |

|

|

Gross profit (loss), rub. |

|

|

Profit (loss) from sales, rub. |

|

|

Other expenses, rub. |

|

|

Profit (loss) before tax, rub. |

|

|

Current income tax (20%), rub. |

|

|

Net profit (loss), rub. |

So, the revenue of Alpha LLC for 2016 was from the sale of 4,640 chairs at a price of 24,000 rubles per unit. - 111,360 thousand rubles. Production and sales costs amounted to 89,494 thousand rubles.

We subtract the full cost from the revenue and get a profit from sales - 21,866 thousand rubles. Net profit (less taxes and other expenses, the main indicator of the effective functioning of the enterprise) is equal to 17,493 thousand rubles.

When analyzing absolute indicators, net profit is not the only thing worth paying attention to. No less important is the ratio of sales revenue to production costs.

If the level of product costs and revenue from its sales are approximately equal, the enterprise will receive little profit, so it must strive to obtain more revenue at lower costs. Thus, we can conclude that an enterprise can be considered profitable if its revenue from sales of products is sufficient to cover all costs of production and sales of products and to create a difference, i.e. profit.

After the absolute indicators of profitability, we analyze the relative indicators - profitability, i.e. indicators of the economic efficiency of the enterprise.

Product sales profitability (ROM, Returnon Margin) - the ratio of profit (loss) from sales to cost.

In our case ROM= 21,866,258.36 / 89,493,741.64 x 100% = 24.43%.

Important!

The higher the profitability of product sales, the more efficient the production and sales of products, and therefore the higher the competitiveness of the enterprise. To increase this indicator, it is necessary to reduce the cost of production and sales of products and increase sales volumes.

Return on sales (ROS, Margin on sales) - the ratio of profit (loss) from sales to revenue.

In the example under consideration ROS= 21,866,258.36 / 111,360,000.00 x 100% = 20%.

As we can see, the values of the profitability and competitiveness indicators of the analyzed enterprise are quite large (the minimum minimum profitability is 5%).

The cost includes all the costs incurred by the enterprise for the production of these products and their sale. They are grouped into two large categories: conditionally permanent And conditional variables.

The first (Table 2) do not depend or weakly depend on the volume of production (for example, depreciation charges, rent for premises, wages of personnel not related to production, purchase of office supplies, information and consulting costs, expenses for telephony, Internet, etc. ), the latter (Table 3) directly depend on volume, i.e. they either increase with an increase in production volume, or decrease with its decrease (for example, costs of raw materials, wages of main production workers, etc.).

table 2 Conditionally fixed expenses for 2016

|

Index |

Value, rub. |

|

Rent |

|

|

Public utilities |

|

|

Depreciation deductions |

|

|

Labor costs |

|

|

Insurance premiums |

|

|

Total |

16 850 180,04 |

The amount of semi-fixed expenses for 2016 is RUB 16,850,180.04. Regardless of changes in production volume, it will remain at the same level.

Table 3 Conditionally variable expenses

|

Index |

Cost per unit, rub. |

Total |

|

Sales volume, pcs. (units) |

||

|

Material costs, rub. |

||

|

Expenses for remuneration of main production workers, rub. |

||

|

Total |

15 655,94 |

72 643 561,60 |

Taking into account the standards for the consumption of materials and the cost of remunerating the main production workers per chair, the amount of semi-variable costs for the entire volume of production (4640 units) was calculated - 72,643,561.60 rubles.

The sum of semi-fixed (RUB 16,850,180.04) and semi-variable expenses (RUB 72,643,561.60) gives a valuation of the total cost (RUB 89,493,741.64; see also Table 1).

Let's calculate the permissible production volume at which the enterprise will cease to be profitable, but will not become unprofitable - break-even point.

The break-even sales volume is 2,019 chairs. With such a quantity, the enterprise will receive neither profit nor loss, and only starting from 2020 units. the company will begin to make a profit. In this case, the amount of semi-fixed (16,850,180 rubles) and semi-variable expenses (15,655.94 x 2019 = 31,609,342 rubles) is approximately equal to the amount of sales revenue (2019 x 24,000 = 48,456,000 rubles. ), in this situation there will be neither profit nor loss.

The difference between the planned sales volume and break-even is called strength threshold. In our example, this is 2621 units. It is necessary to monitor this indicator and not allow it to approach zero.

At this point we cover all expenses - both semi-fixed and semi-variable, and each next unit of production sold will bring approximately 8,344 rubles. profit (24,000.00 – 15,655.94).

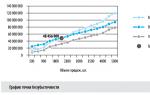

For greater clarity, let’s draw up a break-even chart based on the initial data (Table 4).

In this graph, the values of costs (total, variable) and revenue are located vertically, and the values of sales volume are located horizontally. The graph shows that with a value of 2019 units. the lines of revenue and total costs intersect, which indicates that at this point their values are equal.

For all sales volumes below 2019 units. the cost line exceeds the revenue line, therefore, the enterprise is unprofitable; at values above 2019 units. the revenue line exceeds the cost line - the enterprise makes a profit.

Methods to increase profitability

The main factors that a company can influence are: increase in sales, increase in unit selling price And cost reduction.

Option 1

We will increase sales volume from 4640 units. up to 5,000 chairs per year, subject to demand for such a quantity in the sales market and maintaining the current number of employees without expanding production.

Revenue = 5000 x 24,000 = 120,000,000 rub.

Conditionally fixed expenses = RUB 16,850,180.04.

Conditionally variable expenses = 5,000.00 x 15,655.94 = 78,279,700 rub.

Profit from sales = 120,000,000 – 16,850,180.04 – 78,279,700 = 24,870,119.96 rubles.

Conclusion

By increasing our sales volume by 360 chairs and maintaining the same sales price per unit, we received an additional profit of RUB 3,003,861.60.

Option 2

We will increase the cost per unit of production to 25,000 rubles. All other things being equal, the situation will be similar to the previous one. Revenue will increase and amount to RUB 116,000,000. (25,000.00 x 4640) while maintaining the same level of conditionally fixed and conditionally variable costs.

Conclusion

In this case, the profit will be 26,506,258.36 rubles. (116,000,000 – 89,493,741.64), which exceeds the profit value at a unit cost of 24,000 rubles. for 4,640,000 rubles.

Both in the case of an increase in sales volume and in the case of an increase in price, it is necessary to take into account the nuances. There are no guarantees that, for example, the enterprise will be able to realize the increased production volume - it is quite possible that the market does not need such quantity. And then the enterprise, which has already spent money on producing a larger quantity of products, which, moreover, could not sell, will be forced to bear the costs of organizing/renting a larger warehouse for finished products. And if the products are perishable, the enterprise will also incur losses with such an increase in production. To avoid such situations, you need to carefully analyze the market and potential buyers.

As for the increase in the price per unit of production: when, other things being equal, the properties of the product (quality, design, etc.) its cost increases, buyers may refuse to purchase the product. This situation can also be aggravated by comparison with competitors' prices.

We found that the profitability of any enterprise is affected by changes in the balance of unsold products, as is the case with an increase in production volume with a constant sales volume. The remainder (360 units that will not be sold) is an incomplete receipt of revenue, therefore, no profit received from the funds already spent on the production of these 360 chairs.

To increase the level of profitability and profitability, the enterprise needs to reduce the balance of unsold products.

And finally, we move on to the most common way to increase profitability - reducing production costs. To reduce production costs, enterprises often develop methods and programs to implement certain measures. But first it is necessary to study the cost structure item by item and determine the specific weight of each item (Table 5).

Table 5 Composition and cost structure

|

No. |

Index |

Value, rub. |

Share, % |

|

Rent |

|||

|

Public utilities |

|||

|

Telephone and Internet expenses |

|||

|

Depreciation deductions |

|||

|

Labor costs for management personnel and engineers |

|||

|

Insurance premiums for management personnel and engineering staff |

|||

|

Material costs |

|||

|

Labor costs for key production workers and insurance premiums |

|||

|

Total |

89 493 741,64 |

||

In the price structure, the largest share is occupied by two cost items - “Material costs” and “Costs for remuneration of main production workers and insurance premiums.” It is rational to start reducing production costs with them.

Ways to reduce costs under the item “Payment costs for key production workers and insurance premiums”:

- reduce the number of employees (for example, by automating some processes);

- reduce wages. But this may entail the departure of highly qualified specialists. Therefore, various motivation systems and progressive remuneration systems are usually used so that production workers perform a larger volume of work for the same level of wages.

Option 3

We will reduce the number of key production workers by 10 people, subject to the automation of some production processes.

The total number of employees before the reduction was 80 people.

On average, per year for each person under the item “Expenses for remuneration of main production workers and insurance premiums” there are 617,940.12 rubles. (with an average salary of about 50,000 rubles). In the event of a reduction in numbers, expenses under this item will be equal to RUB 43,255,808.40.

But at the same time, new equipment will be purchased for automation, which will increase the cost item “Depreciation” by 10% and amount to 57,015.68 rubles.

Conclusion

The cost will be 83,319,523.68 rubles, profit - 28,040,476.32 rubles.

The labor cost item was reduced by 7%.

The most important area of cost reduction for material-intensive industries is savings under the cost item “Material costs”:

- introduction of new technologies;

- the use of waste-free technologies or the use of production waste;

- purchase of cheaper raw materials;

- change of raw material suppliers;

- discount system from a regular supplier of raw materials.

The most common ways to reduce costs under the item “Material costs”:

- reducing the purchase cost of raw materials by concluding contracts with manufacturers directly, bypassing intermediaries or shortening their chain;

- purchasing materials in large quantities. In this case, you can get a discount from the supplier and save on transportation costs. But for this, the company must have available funds - to purchase large quantities and to store these stocks. Therefore, it is imperative to compare the costs of placing large quantities of materials with the benefits of their acquisition;

- independent production of some materials. But there are pitfalls here too: independent production is not always profitable and it is often more expensive to produce it yourself than to buy a finished product from a supplier;

- purchasing cheaper raw materials is the most common way to reduce material costs. At the same time, it is worth paying attention to the quality of the purchased raw materials: with such a reduction in costs, the quality of the finished product may suffer, and this can lead to a loss of demand and, as a result, a decline in profitability.

Option 4

The company purchases cheaper raw materials.

For 1 chair, raw materials and materials are consumed for 5001.80 rubles. (Table 6).

According to the analysis carried out by the logistics department, it is possible to change some suppliers with a more favorable pricing policy, as can be seen from table 6 (columns 7–8 of table 6). Then the cost per unit of production will be reduced by 356.00 rubles, the savings for the entire volume will be 1,651,840.00 rubles. (4640.00 x 356).

Conclusion

The company will make a profit:

11,360,000.00 – 16,850,180.04 – 4,640.00 (10,655.94 + 4,645.80) = 23,509,746.36 rubles.

In addition to the considered methods for reducing costs, reducing overhead costs is considered no less effective: they are not directly related to the production of products and their reduction will not affect the production process and/or the quality of the products.

We have examined the most common methods of increasing profitability; now we will conduct a comparative analysis of the effectiveness of their use (Table 7).

Table 7 Comparative analysis of the effectiveness of various methods of increasing profitability

|

Method of increasing profitability |

Revenue, rub. |

Cost, rub. |

Profit, rub. |

|

Initial data |

|||

|

Increase in sales |

|||

|

Increase in retail selling price |

|||

|

Reduction of the cost item “Payment” |

|||

|

Reducing the cost item “Material costs” |

As we can see, the most profitable method turned out to be to reduce labor costs as they have the largest share in the cost of production. Its implementation allows you to increase profits by 30%.

To achieve the same profit result, it would be necessary to increase sales volume from 4640 units. up to 5400 units or increase the retail price from 24 to 26 thousand rubles. Meanwhile, an increase in sales volume implies additional costs for expanding production, hiring additional workers, and the question remains whether such a number of chairs will be in demand on the market. In addition, an increase in price may lead to the loss of some buyers.

Thus, the most rational method is to reduce costs based on the results of an analysis of absolute profitability indicators.

Now let's see how the proposed methods will affect the indicators of profitability of product sales and profitability of sales (Table 8).

As a result of the implementation of any of the methods, indicators improve, reaching a maximum as a result of reducing costs under the cost item “Payment”. This means that the enterprise's production will become more efficient, and the enterprise itself will become more competitive.

The most effective method for reducing costs for an enterprise is under the “Payment” item, which was implemented by automating part of the production processes.

conclusions

It is important to keep your finger on the pulse regarding the profitability of the enterprise and search for ways to increase it.

Let us remind you that the following factors influence the level of profitability:

- unit sales price. It must be at the level of competitors and correspond to the payment capabilities of buyers. To increase profitability, they use the method of increasing the selling price, which, accordingly, increases sales revenue and profit;

- the volume of product sales directly related to the level of demand in the sales market. The planned production volume must correspond to the demand for products: there is no point in producing much more than what the market requires (except in the situation of building up stocks of finished products). To increase profitability, they increase production volumes and look for new channels for selling products, thus increasing revenue;

- cost of production. If the cost exceeds the revenue from sales of products, the enterprise will become unprofitable. To increase profitability, they try to reduce costs while keeping sales revenue constant.

The most effective method is to reduce the cost of production, since there is no guarantee that the product will be purchased at an inflated price or will be purchased in larger quantities.

When implementing a cost reduction method, it is worth considering several important aspects, the main one of which is that the quality of products must not be allowed to deteriorate by reducing production costs.

In addition, it is worth remembering that when choosing this method of increasing the level of profitability, it is recommended to reduce costs in several areas (for example, according to the cost items “Labor” and “Material expenses”, expenses for which, according to statistics, have the largest share in the cost of production). This will allow you to achieve the maximum effect from the implementation of the method under consideration: increase the level of profitability, reduce the selling price of a unit of production, and therefore ensure greater competitiveness and attract more potential buyers.

INTRODUCTION 3

1. THEORETICAL ASPECTS OF PROFITABILITY OF A TRADING ENTERPRISE 5

1.1 Economic essence of income of a trading enterprise 5

1.2 Formation and use of income from sales of products (works, services) 9

1.3 Profitability as an indicator of enterprise profitability 15

1.4 Ways to increase the profitability of an enterprise 16

2. ANALYSIS OF ECONOMIC ACTIVITY INDICATORS OF A TRADE ENTERPRISE 20

2.1 Organizational and legal characteristics of the activities of the Nessky Consumer Society and the main areas of activity 20

2.2 Analysis of income of the Nesssky Consumer Society 24

CONCLUSION 34

REFERENCES 36

APPENDIX 1 38

INTRODUCTION

In the process of supply, production, sales and financial activities, a continuous process of capital circulation occurs, its structure and sources of formation, the availability and need for financial resources and, as a consequence, the financial condition of the enterprise, the external manifestation of which is solvency, change.

Analysis of the profitability of an enterprise allows us to draw a general conclusion regarding the effectiveness of its activities: profitability of capital investment and optimality of costs incurred. A system of profitability indicators is also revealed, which allows for a comprehensive assessment of the effectiveness of asset management and profitability of activities.

The versatility of the problems associated with increasing the profitability of a trading enterprise determines the relevance of the study.

The purpose of the study is to study the concept of profitability of a trading enterprise, to study the financial condition and profitability of the Nessky Consumer Society to identify reserves for their improvement.

The goal of the study is achieved as a result of solving a certain interrelated set of analytical problems:

formulating the concept of profitability of a trading enterprise;

performing an analysis of the financial condition of the enterprise;

identifying reserves to increase financial stability and profitability.

The object of the study is the Nessian consumer society.

The subject of the study is the financial processes that determine the profitability of a given trading enterprise.

The first chapter presents the theoretical aspects of the concept under study.

In the second chapter, the characteristics of the enterprise under study are given, an analysis of profitability indicators is carried out and measures are proposed to increase it.

The research method is a systematic approach, in which any system (object) is considered as a set of interrelated elements.

The methodological basis of the study was the works of Russian and foreign economists, publications in periodicals on the problem under consideration.

The practical basis of the study was the reporting data for the Nessky Consumer Society enterprise.

1. THEORETICAL ASPECTS OF PROFITABILITY OF A TRADING ENTERPRISE

1.1 Economic essence of income of a trading enterprise

In a market economy, represented by the movement of commodity and cash flows, income always appears in the form of a certain amount of money. Income is a monetary assessment of the results of a company’s activities in the form of a sum of money at its direct disposal. It reflects the economic performance of the company's business activities. This means that the condition for obtaining cash income is effective participation in the economic life of society. The very fact of receiving it is objective evidence of such participation, and its size is an indicator of the scale of this participation.

The profitability of an economic entity is characterized by absolute and relative indicators. The absolute profitability indicator is the amount of profit or income. The relative indicator is the level of profitability.

Gross output is considered to be a general indicator of the activity of enterprises and industries, which reflects the extent of their contribution to meeting social needs. Unlike industry, where the term “gross output” is usually used, trade sectors do not produce goods and the value created in them is called gross income (hereinafter referred to as GR). This value is created by the labor of trade workers.

Gross income at the macro level reflects the share of trade in the total prices of consumer goods.

The gross income of a trading enterprise as an economic category in the traditional sense represents a part of the cost of a product, which is intended to cover distribution costs and generate profit. It contains pure products. Net production characterizes the newly created value, which, as in other sectors of the economy, consists of wages and profits (Fig. 1).

Rice. 1. Composition of retail products

The amount of income of a trading enterprise is one of the results of its economic activities. The income of a trading enterprise is the financial basis of its activities.

The economic essence of an enterprise’s income is most fully manifested through the following most important tasks, the implementation of which they ensure:

Reimbursement of all current costs (distribution costs) associated with the implementation of its business activities. The implementation of this task ensures the self-sufficiency of the current economic activities of the trading enterprise.

Ensuring payments of various types of tax payments, ensuring the formation of funds from state and local budgets, extra-budgetary funds. The implementation of this task ensures the fulfillment of the financial obligations of the trading enterprise to the state.

Formation of profit of a trading enterprise, through which funds are formed for production development, additional material incentives for personnel, social payments, payments to property owners, reserve funds, etc. The implementation of this task ensures self-financing of the development of the trading enterprise in the coming period.

Independence, self-sufficiency, self-financing require that the gross income of a trading enterprise exceed the costs necessary to fulfill its tasks, i.e. The gross income of a trading enterprise is the initial prerequisite for the competitive functioning of the enterprise.

According to GOST R 51303–99 “Trade. Terms and definitions "gross trading income is an indicator characterizing the financial result of trading activities and is defined as the excess of revenue from the sale of goods and services over the costs of their acquisition for a certain period of time 1.

The income of an enterprise, from an accounting point of view (according to clause 2 of PBU 9/99), is understood as an increase in economic benefits as a result of the receipt of assets (cash, other property) and (or) repayment of liabilities, leading to an increase in the capital of the organization, with the exception of contributions of participants (owners of property) 2.

To gain a deeper understanding of this definition, it is necessary to understand what is meant by the terms “economic benefits,” “assets,” and “capital.”

The only definition of economic benefits can be found in the Concept of Accounting in a Market Economy of Russia (hereinafter referred to as the Concept), approved by the Methodological Council on Accounting under the Ministry of Finance of Russia and the Presidential Council of the Institute of Professional Accountants on December 29, 1997. In the Concept you can find the concept of “future economic benefits”, by which is meant the potential of property to directly or indirectly contribute to the influx of cash and cash equivalents into the organization (clause 7.2.1) 3. At the same time, it is considered that a property will bring economic benefits in the future if it can be:

– used separately or in combination with another object in the production of products, works, services intended for sale;

– exchanged for another piece of property;

– used to pay off accounts payable;

– distributed among the owners of the organization.

Cash equivalents usually mean highly liquid securities that, if necessary, can be very quickly converted into cash (sold on the securities market) without a significant loss in their value. For example, cash equivalents include government and municipal securities.

Unlike economic benefit, the definition of assets is not contained anywhere at all, even in the aforementioned Concept. In this regard, it seems extremely difficult to define them, referring to regulations. Based on the content of paragraph 2 of Art. 8 of the Federal Law of November 21, 1996 No. 129-FZ “On Accounting”, then assets can be identified with property owned by the organization by right of ownership.

The concept of “capital” is the most complex not only in accounting, but also in economic theory. In this regard, there is no generally accepted definition of capital not only in our legislation, but also in world economic theory. Most often, capital is defined as the property of an organization, free from obligations to third parties.

According to Art. 41 of the Tax Code of the Russian Federation “Principles for determining income”, income is understood as economic benefit in monetary or in-kind form, taken into account if it is possible to evaluate it and to the extent that such benefit can be assessed, and determined in accordance with Chapter 25 of the Tax Code of the Russian Federation 4 .

Thus, the Tax Code of the Russian Federation, as well as PBU 9/99, understands income as economic benefit. However, unlike PBU 9/99, the Tax Code of the Russian Federation does not link economic benefits with an increase in the organization’s capital.

1.2 Formation and use of income from sales of products (works, services)

Various aspects of the production, economic and financial activities of the enterprise are reflected in the system of indicators of financial results. This system is formed by indicators of profit and profitability, as well as gross income - revenue from sales of products (works, services).

In a market economy, the basis for the economic development of an enterprise is profit. Profit indicators become the most important for assessing the production and financial activities of enterprises as independent commodity producers. Profit is the main indicator of the efficiency of an enterprise, the source of its life. Profit growth creates the basis for self-financing of the enterprise's activities, expanded reproduction and satisfaction of the social and material needs of the workforce. At the expense of profits, the enterprise's obligations to the budget, banks and other organizations are fulfilled. Several profit indicators are calculated 5.

The final financial result of an enterprise is balance sheet profit (loss). Balance sheet profit is the sum of profit from sales of products (works, services), profit (or loss) from other sales, income and expenses from non-sales operations. The calculation of balance sheet profit can be presented as follows:

PB=PR+PP+PVN, (1)

where PB is balance sheet profit (loss);

PR – profit (or loss) from the sale of products (works, services);

PP – the same from other sales;

PVN – income and expenses for non-operating operations.

Profit from the sale of products (works, services) constitutes, as a rule, the largest part of the entire balance sheet profit of the enterprise. It is defined as the difference between the proceeds from the sale of products at wholesale prices of the enterprise (excluding VAT) and its full cost. If the cost of production exceeds its value in wholesale prices, then the result of the enterprise's production activities will be a loss. Calculation of profit from product sales can be presented as a formula:

PR = VD–Z pr –VAT, (2)

where VD is gross income (revenue) from the sale of products (works, services) at current wholesale prices;

Zpr – costs of production and sales of products (full cost of production);

VAT – value added tax.

Gross income expresses the completion of the production cycle of the enterprise, the return of funds advanced for production into cash and the beginning of their new turnover. Gross income also characterizes the financial results of the enterprise. At manufacturing enterprises, revenue consists of amounts received in payment for products, work, and services to the enterprise's accounts in bank institutions or directly to the enterprise's cash desk. For trade and public catering enterprises, gross income from the sale of goods is defined as the difference between the sales and purchase costs of goods sold. For non-self-supporting organizations, gross income is income from economic and other commercial activities.

Production costs (Z pr) of sold products (works, services) include the full actual cost of sold products (works, services), i.e. the cost of raw materials, the cost of paying production workers, as well as overhead costs associated with the management and maintenance of production: for the maintenance of management personnel, rent, electricity, maintenance and repairs. Subtracting all these expenses from sales revenue, we obtain profit from the sale of products (works, services), i.e. profit from production activities.

Profit (loss) from other sales is the balance of profit (losses) from the sale of products (works, services) of ancillary, auxiliary and service industries that are not included in the volume of sales of the main commercial products. The financial results of the sale of excess and unused material assets are also reflected here. They are defined as the difference between the sale (market) price of the property and the original or residual value of the property, adjusted for the inflation index.

Income (expenses) from non-sales operations combine various income, expenses and losses not related to the sale of products. This indicator includes:

1) the amount of economic sanctions and compensation for losses. This is the total amount of fines, penalties, penalties and other economic sanctions received and paid, with the exception of those contributed to the budget in accordance with the law. The latter are attributed to the profits remaining at the disposal of the enterprise.

2) income (losses) of previous years identified in the reporting year;

3) losses from natural disasters;

4) losses from writing off debts and receivables;

5) receipts of debts previously written off as bad;

6) income from the rental of property;

7) income received from equity participation in joint ventures;

8) dividends on shares, bonds and other securities owned by the enterprise;

9) other expenses, income and losses attributed in accordance with current legislation to the profit and loss account.

Net profit (NP) is the profit remaining at the disposal of the enterprise. It is defined as the difference between the taxable balance sheet profit (PB") and the amount of taxes taking into account benefits (N"):

CP = PB"–N", (3)

To determine taxable profit, balance sheet profit is increased (decreased) by the amount of excess (decrease) in labor costs of the enterprise personnel engaged in the main activity in the structure of the cost of goods sold compared to their standard value. The following are excluded from the amount of profit received:

– rent payments made to the budget from profits in the prescribed manner;

– income (dividends, interest) received on shares, bonds and other securities owned by the enterprise;

– income from equity participation in other enterprises; profit from insurance activities; other income from non-operating operations; the amount of contributions to the reserve fund and other similar funds, the creation of which is provided for by law; income tax benefits.

The general scheme for the formation and use of profit and net income is presented in Figure 2 6.

Currently, the direction of use of net profit is determined by the enterprise independently. State influence on their choice is carried out through taxes, tax fees and economic sanctions. In the future, a transition from profit tax to corporate income tax is envisaged.

Rice. 2 Formation and use of profit in market conditions

Profit indicators characterize the absolute efficiency of the enterprise's economic activities. Along with this absolute

The assessment also calculates relative indicators of business efficiency - profitability indicators (R).

1.3 Profitability as an indicator of enterprise profitability

Depending on what indicators are used in the calculations, several profitability indicators are distinguished. The numerator usually contains one of three values: profit from sales (PR), balance sheet profit (PB) or net profit (NP). The denominator is one of the following indicators: production costs of sold products, production assets, gross income, equity, etc.

Specifically, therefore, the following indicators are calculated (Table 1).

Table 1

Profitability indicators

|

Name of coefficient |

Calculation formula |

Characteristic |

Normative value |

|

Sales profitability |

|

Shows how much profit is per unit of product sold |

An increase in the profitability ratio indicates an increase in profitability |

|

Accounting profitability from core activities |

Shows the level of book profit |

An increase in the profitability ratio indicates an increase in profitability |

|

|

Net profitability from core activities |

|

Shows how much net profit is per unit of revenue |

An increase in the profitability ratio indicates an increase in profitability |

|

Continuation of Table 1 |

|||

|

Net profitability for all types of activities |

Shows how much net profit is per unit of income of the organization |

An increase in the profitability ratio indicates an increase in profitability |

|

|

Economic profitability |

Shows the efficiency of using all the organization’s property |

An increase in the profitability ratio indicates an increase in profitability |

|

|

Return on equity |

|

Shows the efficiency of using equity capital |

None Must ensure return on investment in the enterprise |

1.4 Ways to increase the profitability of an enterprise

In a market economy, a variety of factors influence the profitability of an enterprise. They can be classified according to a variety of criteria.

Depending on the focus of their activities, they can be grouped into two groups: positive and negative.

Depending on the place of origin, all factors can be classified into internal and external.

All internal factors can be divided into objective and subjective. Objective factors are those whose occurrence does not depend on the subject of management. Subjective factors make up the absolute majority; they completely depend on the subject of management. The profitability of an enterprise largely depends on external factors.

Extensive and intensive factors also influence the profitability of an enterprise.

Extensive factors include factors that reflect the volume of production resources, their use over time, as well as unproductive use.

Intensive factors include factors that reflect the efficiency of resource use 7 .

The listed factors affect profit not directly, but through the volume of products sold and cost.

In the current difficult situation, one of the most important tasks of an enterprise is to find possible ways to avoid bankruptcy and increase profitability. Income growth, which is the main indicator of the break-even operation of an enterprise, depends primarily on reducing production costs, as well as on increasing the volume of products sold, while such products and goods must be produced that meet consumer requirements and are in great demand.

Activities related to improving the use of working time have a significant impact on cost reduction. For many industries that are material-intensive or energy-intensive, the most important area of cost reduction is saving materials and energy resources.

Currently, cost reduction should become the main condition for increasing profitability and profitability of production.

No less important factors influencing the profitability of an enterprise are changes in production volume. The larger the sales volume, ultimately, the more profit the company will receive, and vice versa 8.

Improving the quality of manufactured products can be achieved through many factors, such as technical improvement of production, modernization work, etc. Obviously, the quality of products determines the price level of the enterprise, which significantly affects the amount of profit.

It should also be taken into account that the amount of profit, and therefore the profitability of the enterprise, is affected by changes in the balance of unsold products. In order to increase profits, the enterprise must take appropriate measures to reduce the balance of unsold products, both in quantitative and total terms.

Recently, in the context of the development of entrepreneurship, there have been more opportunities to increase profits through non-sales operations. In this area, financial investments can be the most profitable. Specific directions and structure of financial investments must be the result of a well-thought-out enterprise policy based on a reliable assessment of their effectiveness.

The company can also rent out part of its property and ultimately receive income that increases its gross profit 9 .

From this list of measures it follows that they are closely related to other measures aimed at reducing production costs, improving product quality, and more efficient use of all factors of production.

It is very necessary for an enterprise to determine the so-called break-even point of production and sales of products. The break-even point corresponds to the sales volume at which the company covers all fixed and variable costs without making a profit. Using the break-even point, the threshold beyond which sales volume ensures profitability is determined. Moreover, when determining strategy, the company must take into account the margin of financial strength. Having a large margin of financial strength, an enterprise can develop new markets, invest funds both in securities and in production development 10.

When determining the break-even point and the margin of financial strength, entrepreneurs can plan the amount of profit growth depending on economic success in the production of competitive products and take appropriate measures in advance to change in one direction or another the value of variable and fixed costs.

2. ANALYSIS OF INDICATORS OF ECONOMIC ACTIVITY OF A TRADE ENTERPRISE

2.1 Organizational and legal characteristics of the activities of the Nessky Consumer Society and the main areas of activity

The Ness Consumer Society was founded on June 10, 1918. A consumer society is a voluntary association of citizens and legal entities created on a territorial basis on the basis of membership by uniting its members - shareholders of property shares for trading, procurement, production and other activities in order to meet the material needs of its members. The Company is a legal entity, has an independent balance sheet, current and other bank accounts, a seal and other details. Acts on the basis of its Charter, owns property, can acquire and exercise property rights and perform duties in its own name, and be a plaintiff and defendant in courts.

Citizens and legal entities who have made entrance and share contributions and are accepted into the society are shareholders.

Legal address of the consumer society: 166737, Arkhangelsk region, Nenets Autonomous Okrug, Nes village, st. School 11. The company was created for an indefinite period.

The goal of the company is to satisfy the material and other needs of shareholders.

The management bodies of the company are currently: the general meeting of the company - the highest body; The Society Council is a legislative body; The board of the company is the executive body. The control body is the audit commission.

The general meeting of the company has the authority to resolve all issues related to the activities of the company. The Society's Council is accountable to the General Meeting and resolves all issues related to the company's activities during the period between meetings. The board of the company is an executive body and is accountable to the Council of the company.

The basis of economic activity is his property, which belongs to him as a legal entity.

The sources of formation of the company's property are:

– entrance and share fees;

– income from the company’s business activities;

– property that comes into its ownership upon creation of a company;

– income received from placing his own funds in banks, securities;

– funds received from other sources not prohibited by the legislation of the Russian Federation.

The objects of the company's property rights are property complexes, buildings, structures, equipment, raw materials, money, and securities.

The basic principles of conducting economic activities of the company are:

– break-even for society as a whole;

– democratic management;

– financial and economic discipline;

– responsibility of the chairman of the company’s council, members of the company’s council, chairman of the company’s board and members of the company’s board for the results of the company’s economic activities;

– obligatory informing of shareholders by the Council of the company and the board of the company about the results of the economic activities of the company.

Main activities of the Nesssky Consumer Society:

– production and sale of bread and bakery products;

– retail trade of food and industrial goods;

– public catering;

– provision of household services.

The average number of employees in the Nessky Consumer Society in 2009 was 46 people.

Currently, the company unites about 700 shareholders and serves about 1.6 thousand people.

The diagram of the organizational structure of the Ness consumer society is clearly illustrated in Fig. 3:

Rice. 3. Organizational structure of the Nessky Consumer Society

The Ness Consumer Society includes 3 shops, 2 bakeries, a cafe, a hairdresser, and a sewing workshop.

Bakeries bake bread, bakery and confectionery products. Bread and bakery products are sold in consumer society stores to the population of the village. Nes and the village of Chizha, as well as children's and educational institutions and health care institutions.

All work with suppliers is carried out by the trading department of the Nessky Consumer Society. The trading department reports to the Chairman of the Trade Board. The department in its work is guided by the laws of the Russian Federation and the charter of the Nessky Consumer Society. In the trade department there is a mandatory assortment list of goods, which is approved by the Nessky Consumer Society, the administration of the village council, and the sanitary and epidemiological station.

When working with suppliers, Nessky Consumer Society uses various forms and terms of delivery.

Nesskoye Consumer Society enters into contracts for the supply of goods with manufacturing and intermediary companies located in Arkhangelsk, St. Petersburg, Yaroslavl, as well as trade agreements with individuals. It works with many regular suppliers of the Nesssky Consumer Society on a consignment basis, i.e. it receives goods for sale with subsequent payment. The main suppliers are presented in Table 2.

table 2

Information about suppliers of the Nessian Consumer Society for 2009

|

Foodstuffs |

Industrial goods |

|

|

OJSC "Arkhangelsk Meat Processing Plant" |

LLC "Wyss - Petersburg" |

|

|

IP Panikhidina |

Arkhangelsk upholstered furniture factory" |

|

|

Proviant Plus LLC |

"Arkhangelsk Textile Company" |

|

|

PE Zamyatin |

Galar LLC |

|

|

Dolina LLC |

||

|

IP Kuznetsov |

||

|

"Kotlas Poultry Farm" |

The main buyers of products are children's institutions and healthcare institutions for non-cash payments, and the population for cash payments.

The Company's main competitors in rural areas are private entrepreneurs who have certain advantages. One of the competitive advantages is pricing flexibility. Other advantages of competitors include: tax benefits, the ability to quickly adapt to changing market requirements; acceptable work hours for customers (although the society is working to improve the operating hours of trade and public catering establishments and open 24-hour businesses). This all contributes to an increase in the turnover of retail trade and public catering, meeting the demand of shareholders and rural residents, job growth, as well as ensuring the safety of goods by accelerating turnover). The disadvantages of competitors' work include: non-compliance with sanitary requirements, insufficiently high level of quality of service, weak material and technical base.

2.2 Analysis of the income of the Nesssky Consumer Society

Let us analyze the composition and dynamics of the profit of Nessian Consumer Society based on the profit and loss statement f. No. 2 for 2009, the results are presented in Table 3.

The analysis uses the following profit indicators: balance sheet profit, profit from sales of products, works and services, profit from other sales, financial results from non-operating operations, taxable profit, net profit.

Balance sheet profit includes financial results from sales of products, works and services, from other sales, income and expenses from non-sales operations.

Taxable profit is the difference between the balance sheet profit and the amount of real estate tax, profit subject to income tax (on securities and from equity participation in joint ventures), profit received in excess of the maximum level of profitability, withdrawn in full to the budget, costs taken into account when calculation of income tax benefits (measures to eliminate the consequences of the Chernobyl disaster, environmental and fire protection measures, maintenance of children's health camps, nursing homes, etc.).

Net profit is the profit that remains at the disposal of the enterprise after paying all taxes, economic sanctions and contributions to charitable foundations.

Table 3

Analysis of the composition and dynamics of profit of the Nessian Consumer Society

|

Indicator name |

Code page |

2009, thousand rubles |

2008, thousand rubles |

Off |

|

|

+,– |

|||||

|

Gross profit |

|||||

|

Business expenses |

|||||

|

Administrative expenses |

|||||

|

Profit (loss) from sales |

|||||

|

Other income and expenses: |

|||||

|

Interest receivable |

|||||

|

Percentage to be paid |

|||||

|

Other income |

|||||

|

Other expenses |

|||||

|

Deferred tax assets |

|||||

|

Other payments to the budget |

|||||

|

Current income tax |

|||||

Thus, based on the results of Table 2, we can conclude that, compared to the previous year, there is an increase in sales revenue by 4813 thousand rubles, but an increase in cost by 1550 thousand rubles. and an increase in commercial expenses by 3967 thousand rubles. had a negative impact on the sales profit indicator, as a result of which a sales loss in the amount of 723 thousand rubles is determined in the reporting year. A positive aspect is the increase in other income of the organization by 572 thousand rubles, as a result of which the net profit of the Nessky Consumer Society in the reporting year amounted to 650 thousand rubles, however, compared to the previous year, the net profit figure decreased by 20 thousand rubles. Summarizing the above, the company needs to look for ways to increase profitability.

In Table 4, we will conduct a factor analysis of sales profit and determine the influence of each factor.

Table 4

Factor analysis of sales profit

|

Influence of factors |

|||

|

Product cost |

|||

|

Gross profit |

|||

|

Business expenses |

|||

|

Revenue from sales |

|||

|

Index of change in sales volume |

|||

|

The impact of changes in revenue from product sales on sales profit |

|||

|

The impact of changes in the cost level on profit from sales |

|||

|

The impact of changes in the level of business expenses on profit from sales |

|||

|

The impact of changes in the level of administrative expenses on profit from sales |

|||

|

Total change in profit from product sales for the analyzed period |

Thus, based on the results of the resulting table, we can say that the greatest negative impact on the consumer society’s receipt of profit from the sale of products is 2367.94 thousand rubles. impacted by the level of commercial expenses, which means that the company needs to look for ways to reduce commercial expenses to increase the profitability of the organization.

Table 5 shows the structure of gross profit of the Nessian Consumer Society in 2009.

Table 5

Gross profit structure

|

Index |

Line code |

During the reporting period |

Specific gravity, % |

|

Revenue (net) from the sale of goods, products, works, services (less VAT, excise taxes) |

|||

|

Including: Wholesale trade |

|||

|

Retail |

|||

|

Pharmacy |

|||

|

Blanks |

|||

|

Public catering |

|||

|

Production |

|||

|

Household and other services |

|||

|

Other activities |

|||

|

Cost of goods, products, works, services sold |

|||

|

Including: Wholesale trade |

|||

|

Retail |

|||

|

Pharmacy |

|||

|

Blanks |

|||

|

Public catering |

|||

|

Production |

|||

|

Household and other services |

|||

|

Other activities |

|||

|

+,– |

|||

|

including: |

|||

|

Wholesale trade |

|||

|

Retail |

|||

|

Pharmacy |

|||

|

Blanks |

|||

|

Public catering |

|||

|

Production |

|||

|

Household and other services |

|||

|

Other activities |

According to Table 4, we can say that the largest share in the structure of gross profit is occupied by cost - 57.16%, the largest share in sales revenue is occupied by retail trade - 89.27%.

In the production and sale of household and other services, costs exceed income, gross profit is negative, so the enterprise needs to consider the feasibility of this type of activity or look for ways to reduce costs.

The revenue structure is clearly shown in Figure 4.

Rice. 4. Revenue structure of Nessky Consumer Society in 2009

In Table 5, we consider the profitability indicators of the Nessky Consumer Society.

Return on sales is determined by formula 4.

(4)

(4)

Shows how much profit accrues per unit of products sold. An increase in the profitability ratio indicates an increase in profitability.

Accounting profitability from core activities is calculated using formula 5.

Accounting profitability shows the level of book profit. An increase in the profitability ratio indicates an increase in profitability.

Net profitability from core activities is determined by formula 6.

Net profitability from operating activities shows how much net profit is per unit of revenue. An increase in the profitability ratio indicates an increase in profitability.

Net profitability for all types of activities is calculated using formula 7.

Shows how much net profit is per unit of income of the organization. An increase in the profitability ratio indicates an increase in profitability.

Economic profitability is calculated using formula 8.

Economic profitability shows the efficiency of using all the organization’s assets; an increase in the profitability ratio indicates an increase in profitability.

Return on equity is determined by formula 9.

Return on equity shows the efficiency of using equity capital; it should ensure a return on investment in the enterprise.

Table 6

Profitability indicators of Nessky Consumer Society

|

Index |

Indicator value, % |

Change, |

|

|

Return on sales |

(0,040) |

||

|

Accounting profitability from core activities |

|||

|

Net profitability from operating activities |

|||

|

Net profitability for all types of activities |

|||

|

Return on equity |

|||

Thus, according to the results of Table 6, we can conclude that the enterprise has relatively low profitability values, and also tends to decrease, the profitability of the Nesssky Consumer Society is decreasing.

Summarizing the above, we will suggest ways to increase the profitability of the enterprise.

In order to improve its activities by involving the enterprise in the turnover of the enterprise, management needs to implement the following measures:

1) The reserve for growth of enterprise income is the increase in the level of gross profit. Thus, it is necessary to increase the size of the trade margin, having previously examined the pricing policies of competitors. The level of the trade markup should not exceed that of competitors.

2) It is necessary to increase labor productivity, for this it is necessary to make the amount of wages dependent on the performance results of each individual employee, and, if necessary, to optimize the staffing schedule;

3) Since the cost of goods sold has increased significantly in the reporting year, it is necessary to conclude an agreement with the supplier on more favorable terms or change the supplier who will supply goods that are not inferior in quality to those of competitors, but at lower prices;

4) Since the factor analysis of sales profits had a negative impact on the level of commercial expenses, the company needs to reconsider this item of expenses and strive to minimize them;

5) It is necessary to pay attention to the sale of goods with the highest level of gross profit, in particular, to expand their range in accordance with customer requests; carry out a competent advertising policy or ensure sales on insufficiently popular goods;

6) A significant part of the income goes to cover distribution costs, so one of the ways to increase the final profit is the relative savings in the costs of selling goods, so you should pay special attention to the formation of sales costs, trying to minimize them;

7) Improve the organization of labor on the basis of comprehensive rationalization of the trade and technological process.

8) It is necessary to plan profit, constantly analyze the activities of your enterprise, find out the reasons for changes in revenue, gross income, gross profit and normal profit in the previous period.

One of the methods of modern advanced management is an almost daily analysis of the financial condition of the enterprise. This analysis makes it possible to successfully use marginal analysis, the elements of which are demonstrated above, for planning profit and profitability. If generally accepted analysis allows you to successfully conduct business and make high-quality calculations, then the use of limit values allows you to make calculations of future profits with a fairly high degree of accuracy and, based on an analysis of related industries, to timely determine financing priorities for the long term.

CONCLUSION

Self-financing of trade enterprises requires, first of all, the receipt of income from economic activities and, at a minimum, the excess of these incomes over current costs.

The profitability of an economic entity is characterized by absolute and relative indicators. The absolute profitability indicator is the amount of profit or income. The relative indicator is the level of profitability. The income of an enterprise can be classified taking into account accounting, tax and traditional economic approaches, in which there are certain differences.

The specific proportions of distribution and direction of use of income, which are divided into income from ordinary activities and other income, are of great importance for the economic regulation of the economic activity of the enterprise and are determined by it independently, because The financial capabilities of a given enterprise and the direction of its further development depend on the absolute size and ratio of various funds and deductions.

The profitability of enterprises in trade is now most strongly influenced by two factors. In a positive sense, the factor that has not yet passed the commodity famine, which is supported by the stratification of the population by income, and the growing middle class, whose representatives retain sufficient purchasing power. On the negative side, profitability is affected by economic and political instability. Both of these factors negatively affect long-term profit and profitability planning.

An analysis of the financial activities of the Nesssky Consumer Society revealed a decrease in the profitability of the enterprise in 2009; based on the identified problems, ways to increase profitability were proposed.

LIST OF REFERENCES USED

Tax Code of the Russian Federation. Parts one and two. – M.: LLC “TK Velby”, 2009. 512 p.

GOST 51303–99 Trade. Terms and Definitions. IPC Standards Publishing House, 1999

Bakanov, M.I., Theory of economic analysis / A.D. Sheremet – M.: Finance and Statistics, 2007. – 387 p.

Balabanov, I.T. Analysis and planning of finances of a business entity. – M.: Finance and Statistics, 1998. Bernstein L.A. Analysis of financial statements: Translation from English/Scientific editor of translation by corresponding member. RAS I.N. Eliseeva. Ch. ed. series by prof. I'M IN. Sokolov. M.: Finance and Statistics, 2006. – 306 p.

Volkov, O. I. Enterprise Economics / V. K. Sklyarenko: Course of lectures. – M.: INFRA – M., 2003. –280 p.

Gruzinov, V. G. Enterprise Economics / V. D. Gribov: Textbook. allowance. – 2nd ed. add. – M.: Finance and Statistics, 2001. – 208 p.

Novodvorsky, V.D., Sabanin R.L. Accounting and tax accounting of income and expenses. – St. Petersburg: Peter, 2003. 256 p.

Kovaleva, A. M. Firm finances. / M. G. Lapusta, L. G. Skamai. – M.: INFRA – M., 2008. – 416s

Petrov, P.V.

Economics of commodity circulation. / A.N Solomatin. M.: INFRA-M, 2007. – 220 p.

Production management: Textbook for universities/S.D.

Ilyenkova, A.V. Bandurin, G.Ya. Gorbovtsov and others; Ed. S.D. Ilyenkova. – M.: UNITY-DANA, 2000. – 583 p.

Financial management: Textbook for universities / N.F., Samsonov, N.P. Barannikova, A.A. Volodin and others; Ed. N.F. Samsonova. – M.: Finance, UNITY, 1999. – 495 p.

Economics of an enterprise (firm): Textbook / Ed.

|

prof. O. I. Volkova and Assoc. O. V. Devyatkina. |

|||

|

Indicator name |

Code page |

– 3rd ed., revised. and additional – M.: INFRA – M., 2004. – 601 p. |

Enterprise Economics: Textbook for Universities / Ed. prof. V. L. Gorfinkel, prof. V. A. Shvander. – 3rd ed., revised. and additional – M.: UNITY – DANA, 2003. – 718 p. |

|

ANNEX 1 |

|||

|

Revenue (net) from the sale of goods, products, works, services (less VAT, excise taxes) |

|||

|

Including: Wholesale trade |

|||

|

Retail |

|||

|

Pharmacy |

|||

|

Blanks |

|||

|

Public catering |

|||

|

Production |

|||

|

Household and other services |

|||

|

Other activities |

|||

|

Cost of goods, products, works, services sold |

|||

|

Including: Wholesale trade |

|||

|

Retail |

|||

|

Pharmacy |

|||

|

Blanks |

|||

|

Public catering |

|||

|

Production |

|||

|

Household and other services |

|||

|

Other activities |

|||

|

Profit and loss report of Nessian Consumer Society for 2009 |

|||

|

Gross profit |

|||

|

Business expenses |

|||

|

During the reporting period |

|||

|

Profit (loss) from sales |

|||

|

Other income and expenses: |

|||

|

Interest receivable |

|||

|

Including: For similar previous period of the year |

|||

|

Income and expenses from ordinary activities |

|||

|

Gross profit |

|||

|

Percentage to be paid |

|||

|

Other income |

|||

|

Profit (loss) from sales |

|||

|

Other expenses |

|||

|

Interest for using a loan |

Interest on borrowed funds from the population Income from participation in other organizationsProfit (loss) before tax | ||

The coefficient is equal to the ratio of balance sheet profit from sales to the amount of costs for production and sales of products. The initial data for the calculation is the balance sheet.

It is calculated in the FinEkAnalysis program in the Profitability Analysis block as Cost Return on Profit.

Production profitability - what it shows

Shows how much profit an enterprise (organization) receives from each ruble spent on the production and sale of products. This indicator is calculated for the enterprise and for individual divisions or types of products.

Production profitability - formula

General formula for calculating the coefficient:

Calculation formula based on the old balance sheet data:

| K dp = | p.140 | *100% |

| p.020 + p.030 + p.040 |

Where p.140, page 020, p.030, p.040 fields of the profit and loss statement (form No. 2).

Calculation formula based on the new balance sheet:

Production profitability - value

The dynamics of the coefficient indicates the need to revise prices or strengthen control over product costs.

An increase in this indicator in dynamics with a constant value of costs indicates an increase in the volume of trade turnover, therefore, an increase in profit, and vice versa.

Production profitability - diagram

Was the page helpful?

Synonyms

More found about production profitability

- Analysis of enterprise profitability and methods for increasing it

To increase profitability, they increase production volumes and look for new channels for selling products, thereby increasing revenue 2. - Financial analysis of an enterprise - part 2

An unstable financial situation is characterized by a violation of solvency; the enterprise is forced to attract additional sources to cover inventories and costs; there is a decrease in production profitability. However, there are still opportunities to improve the situation. Crisis financial situation - - Analysis of financial condition over time

FFFFC0 >7.561 Profitability of production 1.112 1.24 1.922 2.349 2.42 1.308 Profitability of expenses for ordinary activities 1.023 - Factors and problems of effective use of current assets in the agricultural sector

Violation of price parity is the main reason for the decline in production profitability. Therefore, an effective system of state support for agriculture has been developed abroad. So in countries - Ranking of enterprises in the group

Return on borrowed capital Return on production Return on expenses for ordinary activities of JSC Arsenal EXAMPLE 3.714 7.067 7.826 2.42 - Economic efficiency of the enterprise

The most important cost indicators characterizing the economic efficiency of an enterprise are the volume of gross and marketable output, the size of current expenses and investments in fixed assets, production profitability. Based on economic efficiency indicators, it is possible to determine labor productivity, capital productivity, material intensity, gross and... Based on economic efficiency indicators, it is possible to determine labor productivity, capital productivity, material intensity gross and net income production profitability Increasing economic efficiency The main ways to increase economic efficiency reducing labor intensity saving means of labor increasing - Calculation of the tax burden of an enterprise

However, this method does not take into account indicators of capital intensity, material intensity, labor intensity of products, production profitability and requires additional analysis of the tax burden. Calculation of the tax burden according to Litvin's method... PFS FMS and Social Insurance Fund including deductions for insurance against industrial accidents and occupational diseases % 0 0 4. Rate personal income tax % - Assortment and profit management based on marginal analysis

Let's analyze the profitability of G production from the point of view of marginal income Table 3. Analysis of G production Indicators - Model of automatic financial reporting of an enterprise

We define automatic financial accounting of an enterprise as electronic reporting generated by a calculation module that automatically distributes the proceeds of the main activity to working capital of simple reproduction and income funds of the entities of the enterprise, and the proceeds of non-operating activities to means of expanded production - Analysis of the financial condition of agricultural enterprises in the Altai Territory and ways of their financial recovery

Thus, measures taken at the federal and regional levels undoubtedly contribute to maintaining the financial stability of agricultural enterprises in the region, but in the current difficult conditions more attention is required to increasing the profitability of agricultural production. Conclusions Financial condition is the result of the interaction of all elements of the system of financial relations of an enterprise - Tools for assessing the safety of economic activities of industrial organizations

Profitability and return on sales on average for sugar production organizations in the Voronezh region 2012-2016 Conclusion Summarizing the above - Comparative analysis of methods for assessing the financial position of agricultural producers used by federal and regional banks

The specificity of the activities of enterprises in the agricultural sector is manifested in low business profitability and capital turnover, the seasonal nature of production, the presence of a time gap between the completion of work and - Profitability of production

Analysis and assessment of profitability and profitability Production profitability - what it shows Production profitability reflects the economic efficiency of a business or - Managing the equity of an agricultural production cooperative: problems and solutions

The real level of profitability shows that agricultural production has a low level of profitability and, accordingly, government support is required, which, however, is also typical for - Financial cycle and return on assets of Russian food industry companies: empirical analysis of the relationship

The high profitability of these companies is ensured due to the rapid turnover of inventories resulting from external outsourcing production process - Approaches to assessing the investment attractiveness of an organization: comparative analysis

In our work we will adhere to the following generalized definition where investment attractiveness is a set of characteristics of the economic potential of the enterprise's return on capital, return on assets and investment risk of an economic entity that has a certain ability to... Conventionally, they can be divided into seven main groups production factors financial situation management of the enterprise investment and innovation activities of the enterprise sustainability and legal factors - Production costs of construction products as objects of economic analysis

Profit is a specific goal that every entrepreneur strives for, and production costs are the costs of achieving this goal. The level of profitability of an enterprise is determined by the percentage of the amount of profit received - On final amendments when valuing a business using income approach methods

The first adjustment for the value of non-core and non-functioning assets is determined by the fact that when calculating value using the income approach, only those assets of the organization that are involved in production are taken into account, so they are involved in... But the organization may have assets that are not directly involved in production and then their value will not participate in the generation of cash flow and therefore - Accounting for intangible assets when assessing property complexes for collateral purposes

Intangible assets are necessary in others, it is worthwhile to completely abandon the use of the traditional income approach to valuation. In the example where the object of collateral was planned to be a property complex for the production of optical components - Analysis of methods for assessing the creditworthiness of small businesses in Russian and foreign practice

Marge - margin profitability Purpose - purpose of the loan Amount - size of the loan Repayment - terms of loan repayment... Balance sheet analysis ratio of long-term debt and equity ratio of stable own resources and the amount of assets dynamics of costs and losses compared to production growth rates Analysis of qualitative indicators cash flows Valuation system of analysis France Valuation of the enterprise analysis of it

The economic feasibility of operating an enterprise in a market economy is determined by the receipt of income. The profitability of an enterprise is characterized by absolute and relative indicators. The absolute indicator of profitability is the sum of income and profit. In specialized foreign literature, the concept of “income” is defined as follows:

“Earnings are an increase in economic benefit during an accounting period in the form of an inflow of funds or an increase in the value of assets or a decrease in liabilities, resulting in an increase in capital, unless such growth is provided by contributions from shareholders.”

A briefer concept is defined in the Decree of the President of the Republic of Kazakhstan, which has the force of Law, dated December 26, 1995 No. 2732 “On Accounting”, where Article 13 states: “Income is an increase in assets or a decrease in liabilities in the reporting period.” Without making the appropriate expenses, as a rule, it is impossible to obtain the desired income. Without receiving income, in turn, it is impossible to develop the enterprise and successfully resolve social issues.

Income in a generalized form reflects the results of management, the productivity of living and materialized labor costs. Some economists attribute it to indicators of economic effect, others - to the efficiency of an enterprise. The first ones are right, since the absolute amount of income does not allow us to judge the return on invested funds.

The system of profitability indicators consists, first of all, of absolute indicators of financial results, which include: income from sales of products (works, services), gross income; income from core activities; income from non-core activities; income from ordinary activities before taxes; emergency income; net income, which is the final financial result of the enterprise's activities.

The role of profit in market conditions has increased significantly. As is known, under a planned-directive economy, its role was diminished. Generating income (profit) as an objective function of any enterprise was downplayed. With the transition to a market economy, income (profit) became its driving force. It is he who determines the solution to the fundamental interrelated problems: what to produce, how to produce and for whom to produce. Generating income has become the goal of the functioning of any enterprise, since in a market economy it is the main source of its production and social development. Income growth creates a financial basis for self-financing, which is a prerequisite for successful management, which is a prerequisite for the successful economic activity of an enterprise. This principle is based on full recovery of costs for production and expansion of the production and technical base of the enterprise. It means that each enterprise covers its current and capital costs from its own sources. If there is a temporary lack of funds, the need for them can be met by short-term bank loans and commercial loans, if we are talking about current costs, as well as long-term bank loans used for capital investments.

At the expense of income, part of the enterprise’s obligations to the budget, banks and other enterprises and organizations is also fulfilled. Thus, income becomes the most important indicator for assessing the production and financial activities of an enterprise. It characterizes the degree of its business activity and financial activity of the enterprise. Income determines the level of return on advanced funds and the return on investment in the assets of a given enterprise.